Major funds are probably interested in Bitcoin and altcoins, but four significant hurdles are preventing them from investing.

In an interview with CNBC on June 14, legendary investor Paul Tudor Jones sounded the alarm over advancing inflation. After last week’s consumer price index (CPI) report showed that United States inflation had hit a 13-year high, the founder of Tudor Investment advocated for a 5% Bitcoin (BTC) portfolio allocation.

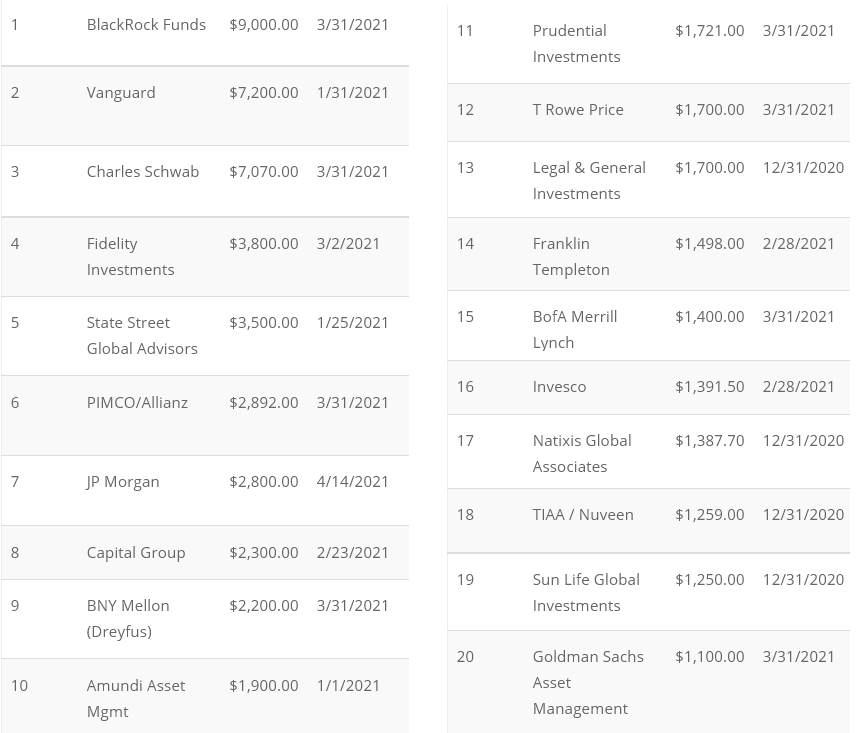

When combined, the world’s 50 largest asset managers oversee $78.9 trillion in funds. A mere 1% investment in cryptocurrencies would amount to $789 billion, which more than Bitcoin’s entire $723 billion market capitalization.

However, there’s a fundamental misunderstanding on how this industry works, and this is what impedes a 1% allocation, let alone a 5% one.

Let’s investigate a few major hurdles that the traditional financial sector will have to vault before really becoming Bitcoin apes.

Hurdle 1: Perceived risk

Investing in Bitcoin remains a significant hurdle for large mutual fund managers, especially considering their perceived risk. On June 11, The U.S. Securities and Exchange Commission (SEC) warned investors about the risks of Bitcoin futures trading — citing market volatility, a lack of regulation and fraud.

Even though several stocks and commodities have similar or even higher 90-day volatility, somehow, the agency’s focus remains on Bitcoin.

DoorDash (DASH), a $49 billion U.S. listed company, holds a 96% volatility, versus Bitcoin’s 90%. Meanwhile, Palantir Technologies (PLTR), a $44 billion U.S. tech stock, has an 87% volatility.

Hurdle 2: Indirect exposure is nearly impossible for US-based companies

Most of the mutual fund industry, mainly the multi-billion dollar asset managers, cannot buy physical Bitcoin. There is nothing specific about this asset class, but most pension funds and 401k vehicles do not allow direct investments in physical gold, art, or farmland.

However, it is possible to circumvent these limitations using exchange-traded funds (ETFs), exchange-traded notes (ETN), and tradeable investment trusts. Cointelegraph previously explained the differences and risks assigned to ETFs and trusts, but that only scratches the surface as each fund has its own regulations and limits.

Hurdle 3: Fund regulation and administrators may prevent BTC purchases

While the fund manager has complete control over the investment decisions, they must follow each specific vehicle regulation and observe the risk controls imposed by the fund’s administrator. Adding new instruments such as CME Bitcoin futures, for example, might require SEC approval. Renaissance Capital’s Medallion funds faced this issue in April 2020.

Those opting for CME Bitcoin futures, such as Tudor Investment, have to constantly roll over the position ahead of monthly expiries. This issue represents both liquidity risk and error tracking from the underlying instrument. Futures were not designed for long-term carry, and their prices vastly differ from regular spot exchanges.

Hurdle 4: The traditional banking industry remains a conflict of interest

Banks are a relevant player in this field as JPMorgan, Merrill Lynch, BNP Paribas, UBS, Goldman Sachs, and Citi figure among the world’s largest mutual funds managers.

The relationship with the remaining asset managers is tight because banks are relevant investors and distributors of these independent mutual funds. This entanglement goes even further because the same financial conglomerates dominate equities and debt offerings, meaning they ultimately decide on a mutual funds’ allocation in such deals.

While Bitcoin is yet to pose a direct threat to these industry mammoths, the lack of understanding and risk aversion, including the regulation uncertainties, cause most of the global $100 trillion professional fund managers to avoid the stress of venturing into a new asset class.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.

Go to Source

Author: Marcel Pechman